Q4'25: The Fog of War

By: Jack Schibli

As a reminder, this blog is an outlet for our thoughts, primarily on the macroeconomic environment, which contextualizes our investments. Please subscribe via the form at the bottom of the page to receive future post notifications.

If you are interested in learning more about our investment strategies, please kindly fill out our contact form here.

TLDR: – "too long; didn’t read." We recognize our posts can be lengthy and challenging to digest, so here’s our executive summary:

- The ongoing cold war between the U.S. and China continues to heat up with plenty of evidence of economic, technological and informational warfare in 2025.

- As a result, military preparations from both sides have accelerated, as the 2027 timeline proposed by Chinese President Xi Jinping nears.

- We believe the world is evolving from an efficiency-based system of hyper globalization and borderless capital to a frictional system based on national security and domestic interests.

- With or without kinetic escalation, the global monetary system is changing. No longer are U.S. dollar surpluses being recycled into U.S. dollar assets, which drove artificially low interest rates.

- Low interest rates drove investors further out on the risk curve, and private and public debt levels to record levels. So, we ask, what if the system that got us here (record equity valuations and high leverage levels) is collapsing?

Cold -> Kinetic 🧊 -> 🔥

For several years now, we have been commenting on the ongoing cold war and believe now is the time for critical updates following many developments in 2025. Stepping back, we must first set the stage. Following China’s admission to the World Trade Organization in 2001, the United States (and Western allies) began the decades long exportation of its manufacturing base to China. Enjoying the fruits of global reserve currency status, the U.S. consistently prioritized the financial economy at the expense of the real, industrial economy. Thus ensued the era of globalization – the increasingly efficient transformation of capital into goods. For most of the 21st century, Western consumers have enjoyed disinflationary access to material goods produced in the East. The U.S. ran persistent, large trade deficits, sending dollars abroad, which came back to the U.S. through the capital account into dollar assets (Treasuries, equities, real estate). Buoyed asset prices, low interest rates, and cheap access to material goods – what more could you ask for?

In Washington, both sides of the aisle have pushed policies favoring the financial economy, which ignored the possibility that America’s access to the material world could be threatened. Today, we fear we stand on the precipice of this becoming a reality – a divorce between capital and production. Three years ago, we wrote about the emergence of a new cold war between East and West, more specifically between the U.S. and China, fought through political, economic, and informational means rather than traditional means. Evidence has been mounting that this may evolve into a kinetic war in the not-so-distant future, which would catalyze a shortage of access to materials and goods as the globalized supply chain fractures in two. Unlike all recent crises, central banks cannot successfully respond by printing, as their printers cannot produce rare earths, base metals, oil, natural gas, or other core inputs to the supply chain. Let’s look at 2025’s developments through the lens of economic, technological, and informational warfare.

Economic:

- After the shock and awe of President Trump’s Liberation Day tariffs faded, it became clear his primary target was China. He sought to hamstring China’s access to the U.S. consumer while leveraging tariff threats with other nations to prevent China from pivoting to new export markets.

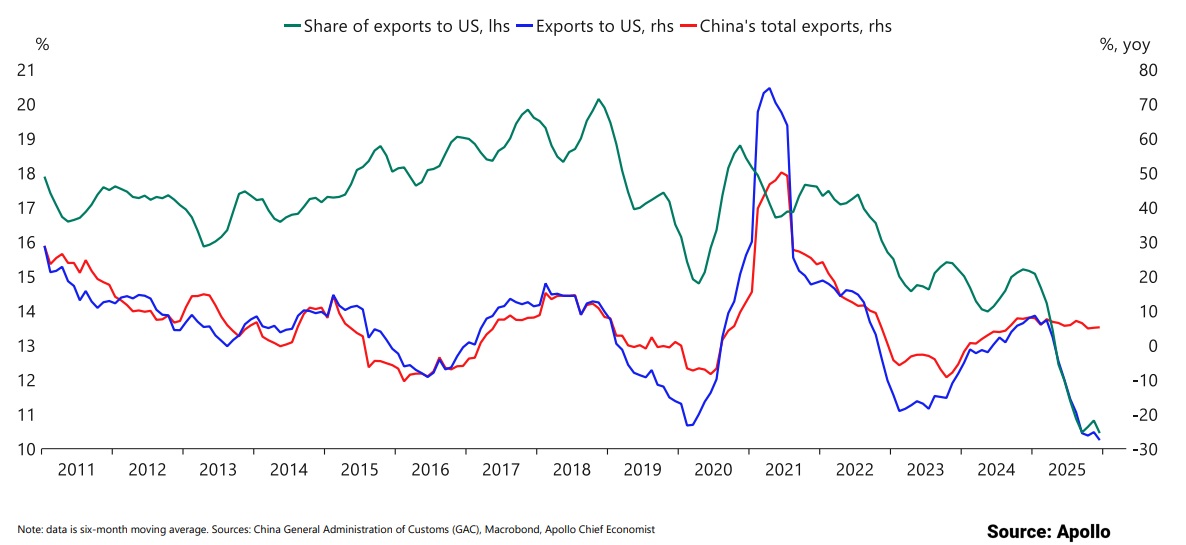

- Tit-for-tat tariffs on specific sectors (and threats of) continued throughout the year, and while the long-term tariff picture remains unclear, the U.S./China trade balance shows signs of decoupling; China’s exports to the U.S. fell 20% in 2025.

- Despite Trump’s efforts, China appears to have found alternative export avenues, as total exports rose 5.5% in 2025. With imports flat, China saw its largest ever trade surplus of $1.2 trillion.

- China responded with tightened export controls on rare earth elements, weaponizing its near monopoly on these critical inputs to semiconductors.

- China also implemented a ban on gallium and germanium (also critical to semiconductors), causing U.S. shortages and forcing workarounds via third-party routing. This ban has been temporarily suspended as of November as part of the latest U.S./China trade “truce”.

- Rising tensions have propelled Trump’s expansionist vision to new heights under the veil of resource securitization. Trump rang in the New Year with the capture of Venezuelan dictator Nicolas Maduro, whose nation is reportedly home to the largest oil reserves in the world. For decades, the Chinese have held strong ties in Venezuela, having lent over $60 billion to them between 2007 and 2015, and been the largest buyer of their oil since 2019, despite US sanctions.

- Next on his list is the conquest of Greenland, home to many critical raw materials and geographically strategically positioned.

- Perhaps unrelated at first glance, but the U.S. bailout of Argentina was designed to retain and strengthen U.S. ties to Latin America, as China has made significant inroads in the continent over the last decade through its Belt and Road initiative.

For Illustrative Purposes Only

For Illustrative Purposes OnlyTechnological:

- Trump has continued Biden-era export controls on advanced semiconductor equipment to impede China’s AI development. After flip-flopping, he then allowed NVDA’s “dumbed down” H20 chip to be sold, but China responded by discouraging its use, insinuating the chip may pose a security threat.

- The U.S. has also pressured the Dutch government, home to chip-making equipment giant ASML, to restrict exports to China to further slow its technological progress.

- Domestically, the CHIPS Act of 2022 authorized over $280 billion in funding to domestic research and manufacturing of advanced semiconductors. Taiwan Semiconductor Manufacturing Co. (TSMC) has built a fab in Arizona, which has entered early stages of production in a U.S. push to reduce reliance on TSMC’s Taiwanese fabs.

- In February, Trump signed a National Security Presidential Memorandum directing the Committee on Foreign Investment (CFIUS) to restrict China-affiliated investors from participating in strategic U.S. sectors, including technology, healthcare, agriculture, energy, and materials.

- Meanwhile, the Chinese government has taken an even stronger “big-brother” role in its AI industry, overseeing and facilitating China’s AI development, whose open-source nature threatens the very existence of U.S. frontier labs.

- In December, Trump signed the 2026 National Defense Authorization act which included the “FIGHT China Act”, banning U.S. investment in Chinese companies involved in military intelligence or advanced technology (AI, quantum, etc.).

- Trump also recently signed the BIOSECURE Act, which bars federal agencies from buying biotech equipment from Chinese “companies of concern”, qualifying even basic lab supplies as security threats.

Informational & Ideological:

- China is a well-oiled propaganda machine, labeling increasing pressure from the West as an attempt to stop China’s great rise. A key focus is Taiwan’s reunification with the mainland.

- Through TikTok, China has its own U.S.-based propaganda machine, which appears to be most heavily used to drive internal distrust and conflict amongst U.S. citizens.

- In 2025, the U.S. uncovered and prosecuted several high-profile Chinese spy cases, including a U.S. Navy sailor (Jinchao Wei) who had been sending technical manuals and ship schematics to his Chinese handler.

- China operates a cyber espionage campaign known as Salt Typhoon, which is reported to access the unencrypted phone calls, texts, and voicemails of almost every American, and in some cases, emails, through the hacking of U.S. telecom networks.

- In fact, in Microsoft’s very own annual 10-K filing, the company reports in its risk section that a nation-state successfully gained access to its emails and source code in late 2023. Shockingly, Microsoft admits that the perpetrator continues to have access, and that the issue has not been resolved.

These lists are not exhaustive but serve to highlight the ongoing silent war between today’s powers. Analyzing President Trump’s actions through this lens, we believe, reveals a common denominator of preparation for a world in which the U.S. is at physical war with China. What might kinetic warfare look like? Well, while there have not yet been any material incidents, there sure have been many preparations:

Military Preparations:

- China capped 2025 with its largest-ever military exercises around Taiwan, simulating an island blockade with live-fire components (following $11.1 billion in U.S.-approved arms sales to Taiwan).

- PLA aircraft and naval incursions into Taiwanese territory are now daily occurrences.

- In a September Chinese military parade, attended by Putin and Kim Jong Un, Xi Jinping’s PLA revealed advanced weaponry, including underwater drones, hypersonic missiles designed to target naval ships, and intercontinental nuclear warheads.

- The U.S. has bolstered military alliances in the Pacific through the advancement of the AUKUS Pact, which expands Australia’s nuclear-powered submarine fleet, and the Quad’s (U.S., Japan, Australia, India) continued preparatory maritime exercises.

- Trump has called for an over 50% increase in the U.S. military budget to $1.5 trillion. He has also threatened bans on share buybacks and limits on executive pay among large U.S. defense contractors to prioritize resource allocation.

- Japan approved a record defense budget for 2026, citing China’s accelerated military buildup and expansion as a threat.

It goes without saying that a kinetic escalation would be detrimental to global supply chains, which have sacrificed resiliency for efficiency. The clock is ticking for companies to align supply chains for this possibility – swapping just-in-time for just-in-case. In Tesla’s most recent earnings call, Elon Musk discussed Tesla’s decision to build a domestic semiconductor fab, citing “I think people may be underweighting some of the geopolitical risks that are going to be a major factor in the next few years”. Given the weighted dominance of large-cap technology companies in the S&P 500, we believe a severely impaired semiconductor supply chain would likely wreak havoc on U.S. equities. How many iPhones could Apple make without access to China? How many GPUs could Nvidia produce without access to Taiwan? These are the types of questions investors should be asking, and perhaps, as consumers, securing your next iPhone before you need it may prove rather prudent.

It is public knowledge that Xi Jinping has instructed the Chinese PLA to be ready to invade Taiwan by 2027. This timeline has U.S. officials concerned and has accelerated preparatory measures. In the White House’s November 2025 National Security Strategy brief (which reads as a U.S. geopolitical manifesto), there is a section entitled Deferring Military Threats, which goes on to state:

“There is, rightly, much focus on Taiwan, partly because of Taiwan’s dominance of semiconductor production, but mostly because Taiwan provides direct access to the Second Island Chain and splits Northeast and Southeast Asia into two distinct theaters. Given that one-third of global shipping passes annually through the South China Sea, this has major implications for the U.S. economy. Hence deterring a conflict over Taiwan, ideally by preserving military overmatch, is a priority”.

Interestingly, there are two annual weather windows – late March to the end of April and September through October – that are most favorable to the Chinese mission, increasing the likelihood that any invasion will occur during these periods. Forgive our superstition, but 2026 is the Chinese Year of the Horse, symbolizing energy, strength, freedom, and independence – the type of horoscope wind you’d like in your sails if you are Xi Jinping.

Monetary Implications 💱

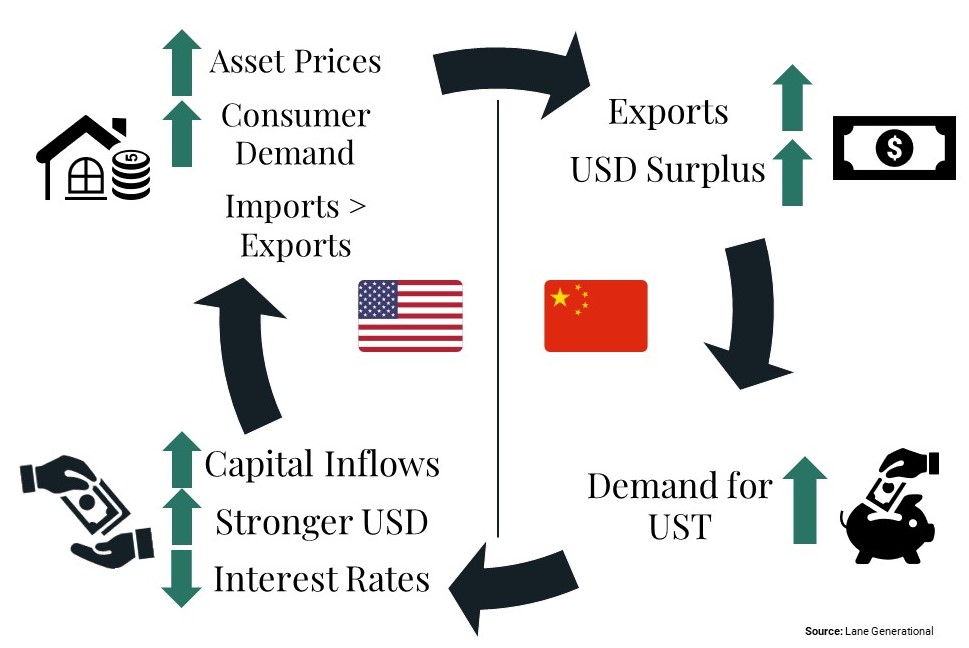

The consequences of conflict between the U.S. and China stretch far and wide, but a key area is the changing global monetary order, which we submit has been underway for several years. We subscribe to Russell Napier’s view that the current monetary system began in 1994, when China pegged its currency to the dollar, and devalued the Yuan to further boost export competitiveness. So began the rise of China’s manufacturing sector, and the flow of goods from West to East meant a flow of dollars from East to West. Chinese trade surpluses were largely recycled into dollar assets, particularly U.S. Treasuries, which kept interest rates artificially low. This unnatural divergence between interest rates and economic growth rates in the West led investors to chase risk assets and leverage for returns, culminating in today’s record equity valuation and record-high debt levels. U.S. corporations enjoyed access to cheap manufacturing in China via a favorably maintained exchange rate, as well as cheap access to capital, combining for a boom in profit margins.

For Illustrative Purposes Only

For Illustrative Purposes OnlyThis unnamed system has created large imbalances in the prices of money and assets in the West, and in China, the focus on supply-side economics has created a deflationary impulse so large that China was forced to announce its largest-ever stimulus package in September 2024. This change in policy appears incompatible with a fixed exchange rate over the long term, and, combined with U.S. corporations diversifying supply chains due to growing geopolitical tensions, we believe it spells the end of this monetary order. A new system will be born, and we suspect it will have significant effects for Western investors. Russell Napier believes the world may fracture into two systems, one Chinese-centric and another U.S. centric. He believes the West will focus on inflating away debt through high levels of forced fixed asset investment, also known as financial repression.

We have already seen the early signs of such a system. The U.S. is prioritizing reshoring manufacturing and directing federal investment into key industries, such as semiconductors, critical minerals, defense, quantum, and biotech. Meanwhile, Europe has awakened to the need for domestic investment. In his 2024 speech “Europe – it can die”, French President Macron highlighted that European savings are being invested in U.S. Treasuries and assets, and instead should be invested in European-based projects that serve the national purpose. This is a coordinated call for the repatriation of capital and the prioritization of domestic interests. These moves are the marks of a deglobalizing and polarizing world in which the national interest (security, prosperity) comes before borderless capitalism.

Investors should consider the implications of such a structural shift, as we believe much of “American Exceptionalism” (and related equity market returns) has resulted from these global imbalances. A large-scale repatriation of capital by international investors is likely to prove a significant headwind to U.S. equity valuations, which currently stand in the 99th percentile as judged by the Cyclically Adjusted PE Ratio. It’s also likely to put upward pressure on long-term interest rates, which comes at a time when the U.S. is refinancing record levels of debt. Additionally, the focus on rebuilding domestic supply chains driven by national security concerns is likely to impart an inflationary impulse as China’s cheap production machine is rebuilt from the ground up with the West’s materially higher input and labor costs. One needs to look no further than the parabolic prices of gold and silver, up 145% and 277% respectively over the last 24 months, to find evidence that change is afoot. Change brings volatility, risk, and opportunity. We believe these decade-long structural shifts will create an environment that bears little resemblance to the last few decades; as such, much of what “worked” may no longer.

Disclaimers

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor's particular investment objectives, strategies, tax status, or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information, and it should not be relied on as such.

No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. All investments include a risk of loss that clients should be prepared to bear. The principal risks of Lane Generational strategies are disclosed in the publicly available Form ADV Part 2A.

This report is the intellectual property of Lane Generational, LLC, and may not be reproduced, distributed, or published by any person for any purpose without Lane Generational, LLC’s prior written consent.

For additional information and disclosures, please see our disclosure page.

Sources:

All financial data is sourced from Refinitiv Data or Federal Reserve Economic Data (FRED) unless otherwise noted.