Q2'25: The Boy Who Cried Wolf

By: Jack Schibli

As a reminder, this blog is an outlet for our thoughts, primarily on the macroeconomic environment, which contextualizes our investments. Please subscribe via the form at the bottom of the page to receive future post notifications.

If you are interested in learning more about our investment strategies, please kindly fill out our contact form here.

The title of our last post – “Smoke and Mirrors” – summarized our view of Trump’s tariff tactics, which later developed into Wall Street’s favorite acronym: TACO = Trump Always Chickens Out. Trump’s heavy and frequent backpedaling helped drive a record rebound in equities during the quarter to new all-time highs. The 90-day trade deal deadline has come and gone with an extension to August 1st, alongside direct letters to trading partners outlining country-specific tariff threats. What’s next in this (exciting? / terrifying?) real-world game of Risk?

TLDR: – "too long; didn’t read." We recognize our posts can be lengthy and challenging to digest, so here’s our executive summary:

- It’s TACO as far as the eye can see. Trump’s walk-back of Liberation Day tariffs has led markets to believe he lacks the spine to follow through on his threats, so why bother taking them seriously?

- China is in the crosshairs of the administration’s strategy to restructure the global trading system, in part because of the improbable but possible reality of a Chinese invasion of Taiwan and related threats to national security.

- We suspect that these geoeconomic games will continue, and Trump is far more serious about playing hardball than the prevailing narrative gives him credit for.

- Meanwhile, Treasury Secretary Scott Bessent has launched a new global financial repression tool via stablecoins and the GENIUS Act, as the administration pivots to a “run it hot” economic playbook.

- Trump is harassing Federal Reserve Chair Jerome Powell, seeking to take the central bank politically captive. We believe this poses a direct threat to the institution's independence and, consequently, the US dollar.

Geoeconomic Statecraft ⚗️

As time has passed, we believe the underlying driver of Trump’s tariff escapade has become clearer. In early 2023, we wrote “A World at War”, outlining the case for an already active East vs. West cold war, fought politically, economically, and financially rather than kinetically. At the heart of this conflict are the global superpowers fighting for future supremacy – the U.S. and China. Tariff developments continue to focus on isolating China. Here are a few illustrative examples:

- Perhaps the most obvious, but not to be overlooked, is the absolute value of the proposed tariffs on China, which is the highest of any country.

- Trump’s recent letters specifically call out “transshipments”, a direct shot at China, which has been attempting to export goods to the U.S. indirectly via hubs such as Vietnam, Thailand, and Mexico.

- Explicitly citing “any country aligning themselves with the Anti-American policies of BRICS, will be charged an additional 10% tariff” and then targeting Brazil – a country the U.S. has a trade surplus (not deficit!) with, and China’s largest trading partner – by threatening 50% tariffs.

- Targeting seemingly inconsequential countries like Myanmar and Laos, which also happen to be key footholds for China’s Belt and Road initiative.

- Slapping the EU with a 30% tariff threat directly ahead of the EU-China summit.

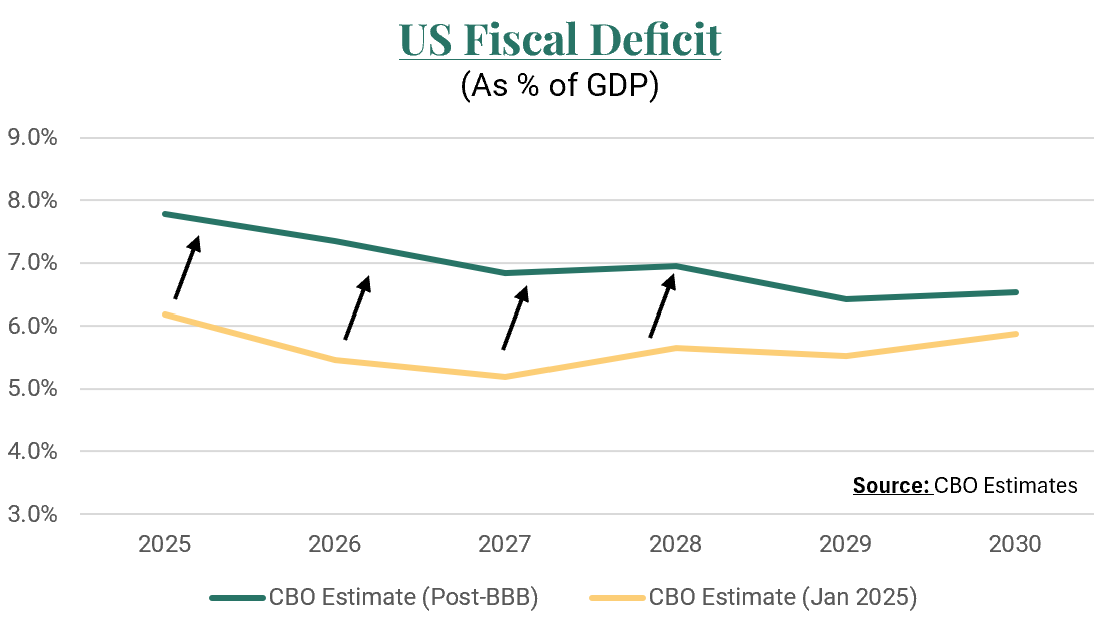

The last bullet point emphasizes Trump’s strategy to use tariffs as a tool to re-establish an allied Western front. In other words, access to the American economy is no longer free; instead, it is contingent upon strategic global alignment. We believe Trump is emboldened – by the passage of the “Big, Beautiful, Bill” (BBB) and equity markets at all-time highs – to possibly shatter the TACO narrative as we approach the new August 1st deadline (or August 12th for China). As shown below, the BBB materially expands the fiscal deficit, a key driver of the economy in recent years; therefore, giving Trump an economic buffer through trade volatility as he re-escalates tariff talks.

For Illustrative Purposes Only

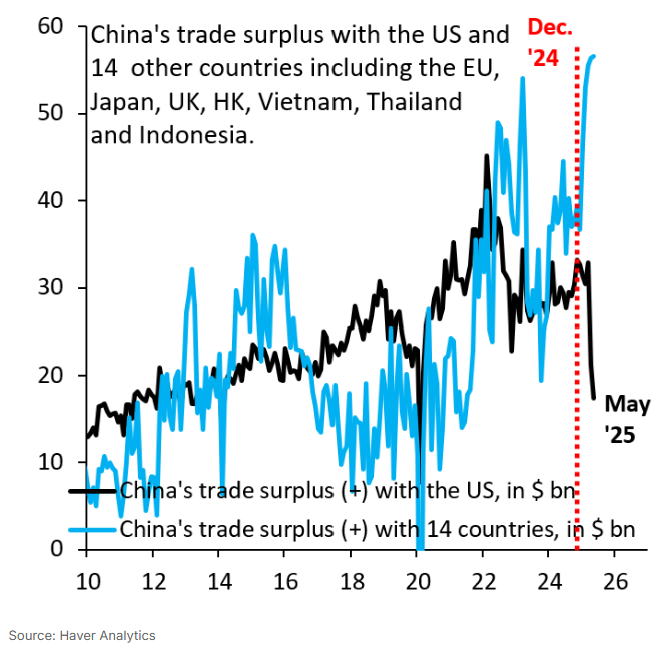

For Illustrative Purposes OnlyThe Chinese are quite clever at finding workarounds and appear to have successfully circumvented Trump’s tariffs for now. The data below shows that the substantial drop in China’s U.S. trade surplus with the U.S. is more than fully offset by a significant increase in trade surplus with a collection of other nations[1]. We assume that many of these nations are being used as transshipment hubs to avoid direct US/China tariff rates.

For Illustrative Purposes Only

For Illustrative Purposes OnlyThe recent spell of tariff letters has not yet directly “re”-targeted China. For now, the U.S. and China have agreed to a framework for ongoing trade discussions, far from the signed “deal” Trump has advertised. The tariff on Chinese imports remains a rather staggering 55%. The U.S. remains heavily reliant on Chinese supply chains for critical rare earth minerals, batteries, and pharmaceuticals. We believe the U.S. is re-architecting its supply chains to prepare for the small but rising odds that it could lose access to these key components of national security from one day to the next in the years ahead.

How? We believe investors are dramatically underestimating the likelihood that Xi Jinping will fulfill his promise of “re-unifying” Taiwan by his stated target of 2027. China continues to prepare in plain sight for an attempted invasion of Taiwan. From a financial perspective, China has decreased its holdings of U.S. Treasuries (in anticipation of sanctions), ramped up gold purchases to a historic pace, and built settlement systems with trading partners outside the U.S. dollar. From an economic perspective, China has been stockpiling critical commodities (amassing 69% of the world’s corn, 60% of its rice, 51% of wheat as of 2022, according to the USDA), diversified suppliers of oil and gas (to heavily include sanction resistant Russia), supported policies that foster greater global reliance on Chinese exports, and mandated state entities abandon foreign-made software. From a legal perspective, Xi has systematically created a legal narrative preempting any conflict over Taiwan as a domestic matter to avoid international law (key legislation includes the 2005 Anti-Secession Law, 2015 National Security Law, 2020 National Defense Law, and 2021 Coast Guard Law). Last but not least, from a military perspective, China has quickly amassed the world’s largest naval fleet, scaled up Air Force training operations into Taiwan’s airspace (conducting 3,615 unauthorized air incursions in 2024 – almost ten per day – up from 972 in 2021), conducted blockade simulation exercises, and even built special purpose barges tailor made for amphibious assault. These lists are not exhaustive but paint a clear picture of deliberate and strategic preparation, analogous to Russia’s multi-year mobilization prior to the invasion of Ukraine.

Perhaps Taiwan remains a distant risk, but the U.S. is likely to employ strategies that maximize deterrence. Therefore, we suspect that the unspoken, yet underlying threat of Taiwan (and the possible ensuing WWIII) will result in continued strain on U.S.-China trade talks. Similarly, discussions with all other trading partners are likely to remain heated as Trump seeks to enforce alignment and expand the East/West divide. Tariffs are his favored tool, as they skirt legislation – though keep an eye on the Court of International Trade’s case claiming Trump’s tariffs are unlawful. We believe Trump’s persona resembles the Strange Case of Dr. Jekyll and Mr. Hyde, an 1886 novel by Robert Louis Stevenson, which contrasts the virtuous Dr. Jekyll with his murderous alter ego, Mr. Hyde. Trump’s version of Mr. Hyde has been dormant since Liberation Day, but it would not surprise us if he were to reappear. He’s already cried wolf – will anyone take him seriously?

Game of Coins 🪙

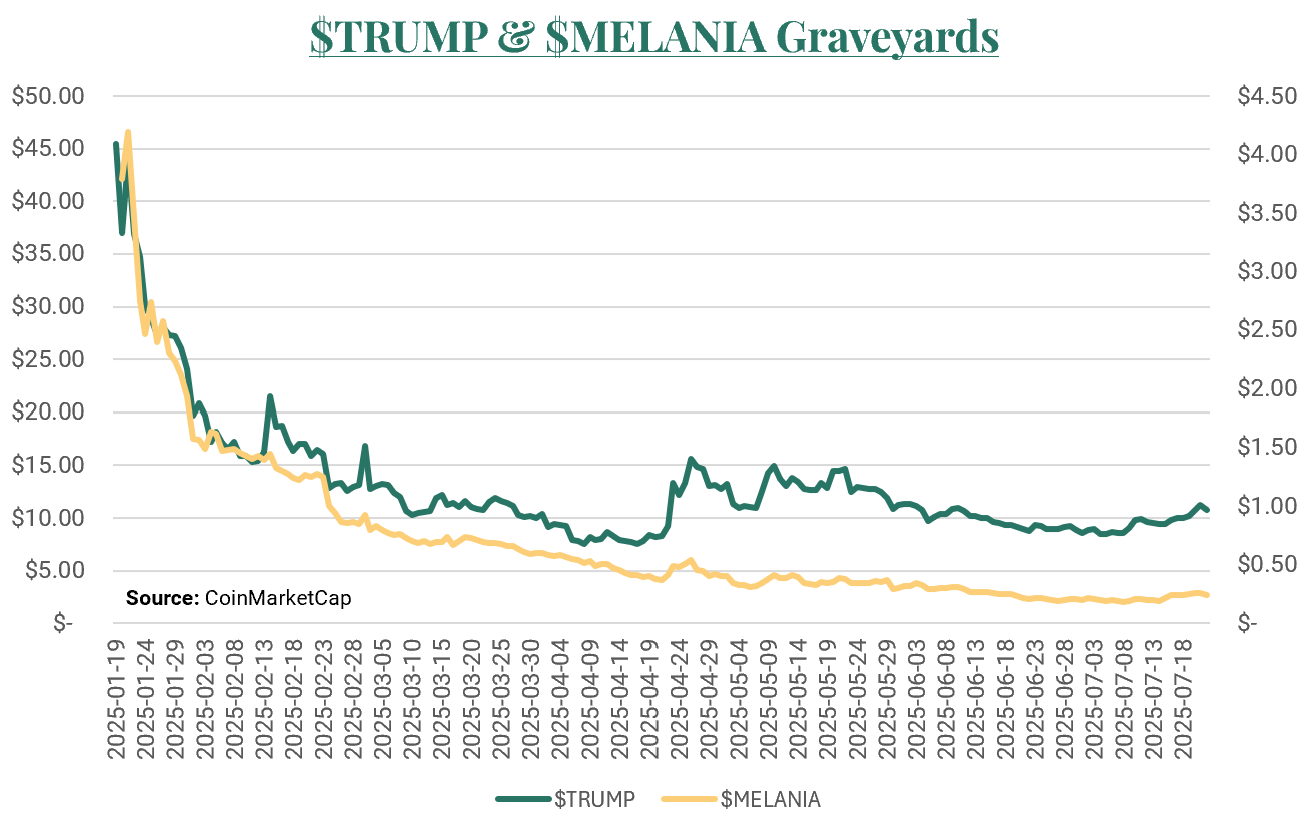

Adding to the list of “unprecedented” developments, Trump is the first U.S. President (and first of any major developed economy for that matter) to openly embrace cryptocurrencies. His green light has marked a fundamental turning point in global adoption levels, which is among the key drivers of price action in a scarce asset such as Bitcoin. Since the election, Bitcoin has gained 69% reaching a recent new all-time high of $120,000 per coin. Many (including us) draw a firm line between Bitcoin and all other “crypto”, but Trump hasn’t – even embracing “meme-coins”, launching $TRUMP coin at his inauguration with wife Melania following suit ($MELANIA). These tokens have zero intrinsic value and fluctuate in value based on sentiment, momentum, Trump’s antics, and possibly even the phase of the moon.

For Illustrative Purposes Only

For Illustrative Purposes OnlyEric Trump has taken to imitating his father’s market timing signals by posting “In my opinion, it’s a great time to add $ETH. You can thank me later” in February. The Trump family is heavily involved with World Liberty Financial (WLF), a “decentralized finance protocol” marketing its own token, $WLFI. The venture's investors include Crypto Chinese Billionaire Justin Sun (who invested $75M, and shortly after the SEC dropped an investigation into him), and an Abu Dhabi-backed firm investing billions into WLF’s new stablecoin, USD1. In addition to the fact that Trump is likely violating the Emolument Clause of the Constitution through his 60% stake in WLF, there appears to be a major ongoing conflict of interest (more on that below).

Trump’s “Crypto Czar”, venture capitalist David Sachs, has been busy pushing for new cryptocurrency regulation, including the recent passage of the GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act). The GENIUS Act establishes a regulatory framework for the use of stablecoins in payments, defined as a digital asset hosted on a blockchain, backed on a 1:1 basis by high-quality liquid assets, such as U.S. dollars and Treasury bills. The bill restricts members of Congress and senior executive branch officials from issuing stablecoins while in public service, but curiously does not restrict the President, who, as noted above, has a stablecoin with billions in foreign backing already on the market. It’s details like these that prompt the question: Is this the Golden Age of Grift? We might fittingly shorten to GAG.

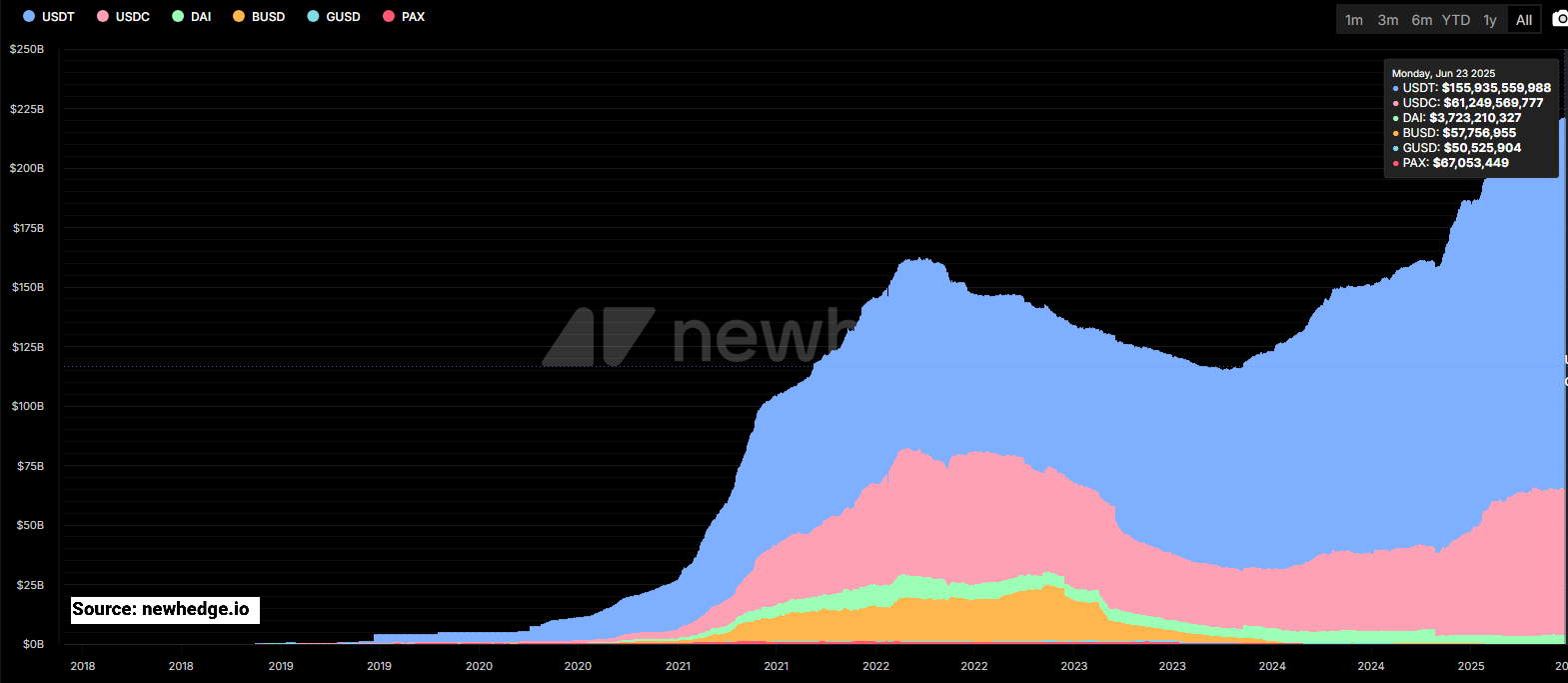

Stablecoins originated as a mechanism to facilitate trading in and out of cryptocurrencies, because dollars in the traditional financial system moved too slowly and lacked 24/7 liquidity. The digital dollars are created by a private issuer who assumes the responsibility of maintaining a peg to the dollar. However, as we have seen many times, pegs have broken materially during times of illiquidity. Currently, the largest issuers are Tether, via USDT (primarily offshore dollars), and Circle Financial, via USDC (primarily domestic). The GENIUS Act will bring stablecoins to payments, and regulation clarity will enable many new issuers, likely to include many of the nation’s largest banks.

For Illustrative Purposes Only

For Illustrative Purposes OnlyWe believe one of the driving factors of this legislation is to create increased demand for U.S. Treasury bills, and Treasury Secretary Scott Bessent has stated as much, given the GENIUS Act requires stablecoin issuers to purchase Treasury securities with maturities less than 90 days. Bessent was a vocal critic of his predecessor Janet Yellen’s issuance strategy, which involved drastically shifting Treasury issuance to short-term bills instead of long-term coupons to loosen financial conditions. Bessent even wrote, “This is a risky strategy…concentrating issuance in short tenors exposes the Treasury to greater volatility via refinancing risks and creates the potential for a financial accident.” However, despite promising otherwise, Bessent has adopted Yellen’s issuance strategy to avoid negatively impacting financial liquidity conditions. Through the GENIUS Act, Bessent appears to have architected a creative workaround to his Treasury issuance troubles.

The U.S. could consider mandating stablecoin settlement in international trade, which would subsequently drive increased foreign demand for stablecoins (and therefore short-term Treasuries). Importantly, stablecoins do not pay interest to the end user, so holders of stablecoins will replace holders of U.S. dollars. Thus, through this mechanism, latent global dollars are being converted into U.S. debt financiers. We believe this constitutes global financial repression, meaning the U.S. Government has just created a new forced, structural bid for its debt, which Bessent has publicized might amount to $2 trillion.

In a major change of heart, the Trump administration has abandoned the promise of deficit reduction through controlling government spending. Elon Musk’s DOGE division has been largely forgotten and overshadowed by the “Big Beautiful Bill”. This pivot marks an admission that our sovereign debt crisis cannot be reined in with austerity but instead must be inflated away. Specifically, this default in real terms is achieved via an extended period of negative real interest rates (when inflation exceeds the interest rate of government debt). Trump and Co. intend to run the economy hot, while artificially suppressing interest rates through repressive policy like the GENIUS Act, and more recently, the public chastising of Federal Reserve Chair Jerome Powell.

What started as typical Trump jabs on his Truth Social page, nicknaming him “Too Late” Powell, has developed into a full-blown coordinated attack. Trump believes the U.S. “deserves” to pay just 1% in interest for short-term borrowing. His frustration with interest rates stems from the fact that interest payments on government debt are now the largest budget line item. Powell has been steadfast in his commitment to hold interest rates at current levels until the economic data provides more clarity on the impact of tariffs on inflation and growth. To his credit, it would also be helpful if we could first receive longer-term clarity on tariffs before attempting to understand their effects. Trump and Co. have aggressively berated Powell, with Federal Housing Finance Administration Director Bill Pulte calling him an “obnoxious, arrogant, pompous person” (we can hardly believe this is real life either). House Republican Anna Luna has even referred Powell to the DOJ for a criminal investigation related to his oversight of the $2.5 billion Federal Reserve building renovation. Rumors have swirled of Trump firing Powell (which requires legal cause) or Powell resigning.

In our view, Trump is actively destroying the last vestiges of trust in the fiat system by attacking the Federal Reserve’s independence. He is politicizing monetary policy to further his agenda, which carries significant risk to the long end of the Treasury curve, as he is removing one of the key tools for managing inflation in the economy. We suspect he may also be building a public narrative to frame Powell as a scapegoat for what could be an impending tariff-induced slowdown. What’s clear is that trust in institutions (including the U.S. dollar) is fading, handily reflected in the charts of Bitcoin and gold, which we have been strong proponents of since the initiation of this blog. Equities at all-time highs seem inconsistent with prevailing short-term risks, but to play devil’s advocate, are they simply reflecting the debasement of U.S. dollar purchasing power? The U.S. dollar has declined by over 10% this year.

Disclaimers

The information provided is for educational and informational purposes only and does not constitute investment advice, and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor's particular investment objectives, strategies, tax status, or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information, and it should not be relied on as such.

Investments involving Bitcoin present unique risks. Consider these risks when evaluating investments involving Bitcoin:

- Not insured. While securities accounts at U.S. brokerage firms are often insured by the Securities Investor Protection Corporation (SIPC) and bank accounts at U.S. banks are often insured by the Federal Deposit Insurance Corporation (FDIC), bitcoins held in a digital wallet or Bitcoin exchange currently do not have similar protections.

- History of volatility. The exchange rate of Bitcoin has historically been very volatile, and the exchange rate of Bitcoin could drastically decline. For example, the exchange rate of Bitcoin has dropped more than 50% in a single day. Bitcoin-related investments may be affected by such volatility.

- Government regulation. Bitcoins are not legal tender. Federal, state, or foreign governments may restrict the use and exchange of Bitcoin.

- Security concerns. Bitcoin exchanges may stop operating or permanently shut down due to fraud, technical glitches, hackers, or malware. Bitcoins also may be stolen by hackers.

- New and developing. As a recent invention, Bitcoin does not have an established track record of credibility and trust. Bitcoin and other virtual currencies are evolving.

No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. All investments include a risk of loss that clients should be prepared to bear. The principal risks of Lane Generational strategies are disclosed in the publicly available Form ADV Part 2A.

This report is the intellectual property of Lane Generational, LLC, and may not be reproduced, distributed, or published by any person for any purpose without Lane Generational, LLC’s prior written consent.

For additional information and disclosures, please see our disclosure page.

Sources:

Unless otherwise noted, all financial data is sourced from Refinitiv Data or Federal Reserve Economic Data (FRED).

[1] Brooks, Robin. China’s transshipment of goods to the US. Brookings EDU. June 2025